UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM ABS-15G

ASSET-BACKED SECURITIZER

REPORT PURSUANT TO SECTION 15G OF

THE SECURITIES EXCHANGE ACT OF 1934

Check the appropriate box to indicate the filing obligation to which this form is intended to satisfy:

| ¨ | Rule 15Ga-1 under the Exchange Act (17 CFR 240.15Ga-1) for the reporting period to |

| Date of Report (Date of earliest event reported) | ||||

| Commission File Number of securitizer: | ||||

| Central Index Key Number of securitizer: | ||||

Name and telephone number, including area code, of the person

to contact in connection with this filing

Indicate by check mark whether the securitizer has no activity to report for the initial period pursuant to Rule 15Ga-1(c)(1) ¨

Indicate by check mark whether the securitizer has no activity to report for the quarterly period pursuant to Rule 15Ga-1(c)(2)(i) ¨

Indicate by check mark whether the securitizer has no activity to report for the annual period pursuant to Rule 15Ga-1(c)(2)(ii) ¨

| x | Rule 15Ga-2 under the Exchange Act (17 CFR 240.15Ga-2) |

Central Index Key Number of depositor: 0001469367

Sunrun Callisto Issuer 2015-1, LLC

(Exact name of issuing entity as specified in its charter)

Central Index Key Number of issuing entity (if applicable): 0001645215

Central Index Key Number of underwriter (if applicable): Not applicable

Mina Kim, (415) 580-6900

Name and telephone number, including area code, of the person

to contact in connection with this filing

Explanatory Note: For purposes of the furnishing of this Form ABS-15G, the Depositors signing below do not have Central Index Key Numbers. The Central Index Key Number listed above of the depositor is the Central Index Key Number of the sponsor, Sunrun Inc.

INFORMATION TO BE INCLUDED IN THE REPORT

FINDINGS AND CONCLUSIONS OF THIRD-PARTY DUE DILIGENCE REPORTS

Item 2.01 Findings and Conclusions of a Third Party Due Diligence Report Obtained by the Issuer

EPC Partners

In total, 47 distinct EPC partners have been used to sell and build the Portfolio’s PV systems. However, the largest three contributors, Verengo, Sungevity, and Sunrun (formerly REC Solar) combine for 65% of the installations and the top 10 contributors combine for 90% of the installations. The Sponsor’s network of EPC partners is somewhat more concentrated than that of several of its competitors, which DNV GL considers potentially advantageous in terms of relationship management for quality assurance purposes and for ongoing warranty support.

The Sponsor’s EPC network has undergone some natural turnover as businesses enter and exit the residential solar market, Sunrun’s platform, and/or are acquired. Several EPC partners contributing to the Portfolio—most notably Verengo, PetersenDean, and Roof Diagnostics—are no longer financing their new PV systems via the Sponsor’s platform. Despite such turnover, the rate of warranty support has been very high to date.

Equipment

The Portfolio contains PV modules and inverters from various suppliers which were approved by the Sponsor at the time each system was purchased from its respective EPC partner. The procurement of the equipment used in the PV systems (aside from monitoring systems) is done by the Sponsor’s EPC partners.

Modules

All PV modules in the Portfolio use crystalline silicon (cSi) technology. By far, this is the most widely deployed and mature technology in the PV industry. Most module suppliers offer a 10-year workmanship warranty and a 97% performance guarantee (degrading at 0.7% per year). Due to the potential difficulty in processing performance-related warranty claims, DNV GL places greater emphasis on ‘out of the box’ quality, such as module design, reliability-related testing and design qualification certificates, manufacturing QA/QC and/or batch testing, and field performance track record. While the solar industry currently lacks a standardized approach for ongoing module QA/QC and reliability testing, historical PV module performance in the U.S. residential solar industry has been relatively strong through about five years to date, with few known warranty recalls occurring in residential solar.

Inverters

All string level inverters are covered by a minimum 10 year warranty. Enphase microinverters have 25 year limited warranties; Enphase does not cover labor cost and has the option to reimburse only the value of the microinverter at the time of failure. String inverters are generally expected to be replaced during the course of the PV system life, with an estimated median life of 12 years. In contrast, DNV GL has reviewed confidential reliability information for Enphase M215 and M250

microinverters which supports a 25 year design life, although some proportion will likely fail over this period. A small proportion of the Portfolio (2%) uses isolated 3.8 / 4.6 kW inverter models from ABB Power-One or older Enphase models (i.e. D380, M190, M210) which have been known to have higher failure rates. The CS XV Fund has seen a relatively high field service dispatch rate in 2014-2015 related to arc fault circuit interrupter (AFCI) trips at systems with ABB inverters, although ABB is covering the cost of these truck rolls under warranty.

Balance of System

The Portfolio predominantly uses approved monitoring systems from Itron, Locus, or Enphase which include a revenue grade meter. Most non-Enphase installations will have monitoring systems which report via a cellular link (as opposed to the homeowner’s internet connection), which has allowed the Sunrun fleet to achieve a historical best 99.75% connectivity rate (within 30 days) as of April 2015.

Sunrun’s EPC partners are free to procure racking and other balance-of-system components at their own discretion, although they are required to meet any local permitting obligations and to comply with EPC Agreement quality standards, which for new installations typically includes compliance with the Installer Handbook.

Warranty

In summary, most inverter warranties generally have a 10-year term starting upon shipment from the factory. In all cases, repaired or replaced components are warranted until the end of the original term, at a minimum. Compensation for labor expense associated with replacing the defective unit varies among the suppliers. The majority of the time, it will be at the supplier’s discretion whether the replacement will be new or refurbished. SMA and Fronius provide an advanced shipment option whereby shipping is paid for and the returned unit can be placed in the same packaging that the replacement unit comes in. Such service is useful for reducing repair downtime.

DNV GL considers the warranty terms strong and a benefit to the Portfolio, particularly the response time requirements and the reimbursement / payment offset provisions in the event that an EPC partner fails to meet them.

The Sponsor has confirmed that as of 31 March 2015, it has paid for EPC partner-responsible warranty work out-of-pocket in just 76 cases (0.6% of the total warranty claims), resulting in just $32k of expenses borne by Sunrun—DNV GL considers this as a positive indication that the warranty provisions have been successfully enforced.

In summary, many of the manufacturers’ leading recent models have been tested to what DNV GL considers essential industry standard performance tests—these models have been included, along with many others, in the Portfolio. DNV GL considers that the risk of design-related performance issues is mitigated to the extent that certified models are used, at least for those bills of materials (BOMs) covered by the third party testing programs. DNV GL notes that Sunrun’s approved equipment list may also contain PV module types other than those modules listed in the above table; Sunrun’s primary consideration for equipment qualification (other than commercial considerations) is inclusion on the CEC list, which requires UL 1703 testing only and therefore does not have the same degree of reliability testing as do modules which also have IEC 61215 certification.

Given that PV module suppliers have faced stiff price competition over the past several years, the manufacturing base of the industry is changing rapidly and there is still some risk of variability in quality across plants and production lines. To the extent that any potential quality issues are not covered by warranty, DNV GL recommends using module replacement estimates and stress cases for the financial model that consider the diversity of the Portfolio, among other factors.

Sunrun Energy Estimate Methodology

The Sponsor’s EPC partners use the PVWatts solar forecasting model within its Proposal Tool (a software platform) to generate PV system energy production estimates. As a simulation engine, the Proposal Tool model sacrifices some accuracy and flexibility in order to increase accessibility and reduce runtime, which is typical for the residential solar industry. The Proposal Tool pulls meteorological data from the overlapping SolarAnywhere 10 km grid tile. DNV GL notes that the uncertainty of the meteorological data is moderately high but is in line with typical industry practice and has the advantage of providing consistency among EPC partners. While DNV GL has not reviewed the PVWatts simulation code, the models employed by the Sponsor are appropriate and should yield accurate energy production estimates given accurate inputs (i.e. meteorological data and loss factor assumptions).

The 25% of systems in the Portfolio which were initiated by Sungevity followed Sungevity’s own forecast process, for which details are not available. For a population of 2,449 systems which had side-by-side Sungevity and Sunrun estimates available, the median ratio of Sungevity-to-Sunrun estimates was 0.991 and the average ratio was 0.996, meaning that on average Sungevity’s estimates were very slightly more conservative than those of Sunrun. In its quantitative energy analysis, DNV GL has considered the slight regional differences in estimation which were observed between Sunrun and Sungevity, and has also (due to lack of specific estimate information and operating history) applied a higher estimate uncertainty for the Sungevity systems.

Overall, based on data from its operating systems, DNV GL notes that the Sponsor’s loss factor assumptions are reasonable and achievable (on average) assuming an active and effective operation and maintenance program. Longer-term degradation has been assessed separately.

In order to validate the EPC partners’ and Sunrun’s level of process consistency with respect to energy estimation, DNV GL has reproduced forecasts for a total of 15 PV systems in the Portfolio, 10 of which were estimated using Sunrun’s processes and 5 of which were estimated using Sungevity’s processes. The level of agreement achieved in these reconciliations leads DNV GL to conclude that the Sponsor’s stated processes have been followed in most cases, with user input errors or other factors leading to variances in some cases which are captured in DNV GL’s analysis of the performance data and uncertainty projections.

IT and Data Management

DNV GL considers the IT and data management systems and procedures implemented by the Sponsor in line with good industry practice. Based on its review of fleet production and service history summaries to date, DNV GL considers that the Sponsor has demonstrated its ability to adequately operate and manage its large portfolio of solar PV systems.

DNV GL Energy Analysis

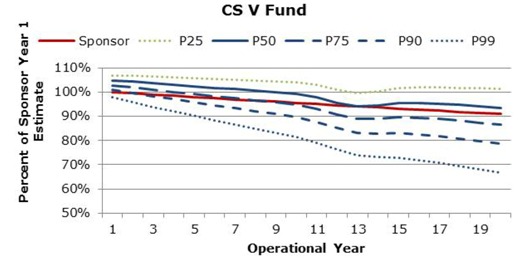

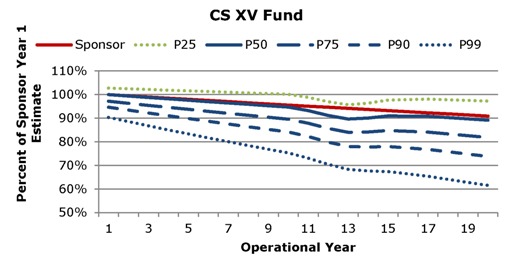

DNV GL has quantitatively evaluated historical system performance against the Sponsor’s methodologies in order to develop Portfolio-specific performance expectations. From this analysis, DNV GL has made the following observations.

| 1. | Overall, to date the Sponsor’s operating systems have outperformed their pre-construction estimates by 6.1% and 0.6%, respectively, for the Previous and Current energy estimate methodologies. The standard deviations of the production ratio with the previous and current methodologies are 10.6% and 8.9%. The relatively high variances in Production Ratio show that while a majority of the PV systems have outperformed their pre-construction estimates, some proportion of the PV systems have not. |

| 2. | DNV GL has separated PV systems on a state-by-state basis. Regional results show similar trends as the entire data set, with most regions showing relatively good agreement between actual and expected production. This highlights that the current energy estimate methodology is effective at determining the mean of distribution of regional systems. The standard deviation of production ranges from 4.7% in Arizona (AZ) to 11.9% in Hawaii (HI), considering regions with a representative sample size. DNV GL notes that the Current methodology regional standard deviations are generally lower than those seen from the Previous methodology. |

| 3. | DNV GL has made adjustments to the production data when necessary to make the results more representative of a long-term Portfolio representative forecast. These are noted in Section 5.2 and include an extension in the system period of record, multiple mounting plane adjustment, and Sungevity adjustment. |

| 4. | For DE, NY and CT, representative samples of production data are not available to compare against energy estimates made by the Sponsor using the Current methodology. For these regions, DNV GL has either estimated appropriate adjustment factors or used neighboring regions as proxies. The uncertainty ascribed to such estimates has been correspondingly increased; this uncertainty can be reduced when representative samples of production data become available. |

| 5. | For any particular PV system, the production estimate is obtained by multiplying the regional correction factor and Sunrun’s estimate. A Fund average correction factor based on the expected regional mix (and mix of Previous methodology, Current methodology, and Sungevity methodology systems) is calculated and shown in the tables below. |

Correction factors for Year 1 and uncertainties for CS V Fund

| Region |

Systems (%) |

Correction Factor |

1-yr Uncertainty1 (%) |

10-yr Uncertainty1 (%) |

||||||||||||

| CA |

71.1 | % | 1.055 | 3.5 | % | 2.2 | % | |||||||||

| NJ |

17.1 | % | 1.034 | 4.7 | % | 2.8 | % | |||||||||

| NY |

0.2 | % | 1.022 | 5.1 | % | 3.4 | % | |||||||||

| MA |

3.9 | % | 1.025 | 4.6 | % | 2.6 | % | |||||||||

| HI |

2.4 | % | 1.054 | 2.9 | % | 2.2 | % | |||||||||

| AZ |

0.4 | % | 1.166 | 1.9 | % | 1.6 | % | |||||||||

| CO |

4.4 | % | 1.026 | 2.5 | % | 2.1 | % | |||||||||

| MD |

0.1 | % | 1.082 | 4.5 | % | 3.0 | % | |||||||||

| PA |

0.5 | % | 0.985 | 5.0 | % | 3.3 | % | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Fund |

100 | % | 1.049 | 3.1 | % | 2.2 | % | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 1. | Uncertainty when Correction Factor is applied to the aggregate forecast for all Portfolio PV systems in the respective region. |

Correction factors for Year 1 and uncertainties for CS XV Fund

| Region |

Systems (%) |

Correction Factor |

1-yr Uncertainty2 (%) |

10-yr Uncertainty2 (%) |

||||||||||||

| CA |

69.9 | % | 1.007 | 4.5 | % | 3.5 | % | |||||||||

| NJ |

2.5 | % | 0.964 | 5.8 | % | 4.3 | % | |||||||||

| NY |

11.0 | % | 0.965 | 6.0 | % | 4.6 | % | |||||||||

| MA |

4.5 | % | 1.012 | 5.6 | % | 4.1 | % | |||||||||

| HI |

3.8 | % | 0.984 | 3.7 | % | 3.2 | % | |||||||||

| AZ |

3.1 | % | 1.005 | 3.1 | % | 3.0 | % | |||||||||

| CO |

0.6 | % | 1.004 | 3.9 | % | 3.7 | % | |||||||||

| DE3 |

1.9 | % | 0.995 | 7.1 | % | 6.0 | % | |||||||||

| CT3 |

1.7 | % | 0.941 | 5.9 | % | 4.8 | % | |||||||||

| MD |

0.9 | % | 0.989 | 6.0 | % | 4.9 | % | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Fund |

100 | % | 1.000 | 4.1 | % | 3.5 | % | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 2. | Uncertainty when Correction Factor is applied to the aggregate forecast for all Portfolio PV systems in the respective region. |

| 3. | Denotes a region where assumption was made due to insufficient production data for empirical result. |

| 6. | Energy estimates for subsequent years were derived by extending the first year forecast over the 20 year forecast period by assuming the degradation and availability loss factors for each respective probability of exceedance case (“P-level”). The regional uncertainty of the forecasts were considered and combined using a portfolio effect analysis, resulting in a 1 year and 10 year total Fund uncertainty as shown in Table 5-20 – Table 5-23. The resulting forecast for each P-level is shown in the figures below, along with the Sponsor’s own estimate. The figures are given in tabular form in Section 5.4.4 and the excel files accompanying this report. |

CS V Fund probabilities of exceedance (one year period) relative to the Sponsor’s base case estimate

CS XV Fund probabilities of exceedance (one year period) relative to the Sponsor’s base case estimate

Customer Agreements

The Portfolio’s individual PPA/Lease contracts provide for the sale of all electricity production at firm pricing ($ per month or $ per kWh) for 20 years. The PPA/Lease contains a clause guarantying that the PV system will produce an amount equivalent to 95% or 100% of the expected output (depending on the contract type). The expected cost of these guarantees is to be borne by the CS V and XV Funds. The homeowner may prepay for the term at any time or opt to purchase the system at select times. If the homeowner sells the site to a new homeowner, they must assign the PPA/Lease to the new homeowner, purchase the PV system, or prepay for the expected electricity during the remainder of the Initial Term. Unlike Sunrun’s lease format, the Sungevity lease (25% of the contracts in the Portfolio) has both a 95% cumulative production guarantee and a clause whereby Sungevity must reimburse its customers for each full day a system is offline; DNV GL has requested details on these leases to assist in quantifying the impact of this refund clause. Otherwise, the PPA/Lease technical terms appear reasonable and do not appear to pose undue risk to the Portfolio.

EPC Agreement

The Sponsor executes a single EPC Agreement to cover work on all PV systems to be delivered by a particular EPC partner. An Addendum is then executed for each individual PV system, containing the technical specifications and any specific terms and conditions for that PV system. DNV GL finds that the EPC Agreement scope of work is adequate and sufficient to facilitate timely completion of a PV system. Quality requirements are clearly established by the Sunrun Installer Handbook; however, such requirements are not contractual under the Sponsor’s old EPC agreement under which most PV systems in the Portfolio were completed.

The work is compensated on a fixed price basis with minimal allowance for change orders. The interfaces between the EPC partner and Sunrun are well defined. Materials and services supplied by EPC partners are warranted against defects for a period of 10 years, while roofing penetrations are warranted for a period of five years. Such terms are consistent with DNV GL’s observations in the broader U.S. market. Sunrun has special requirements to incentivize timely warranty responsiveness, including delay damages of $25 per day starting on the fourth business day after a warranty claim and the ability to offset future payments to an EPC partner to pay a third party to perform the work (in the event the EPC partner fails to respond in a timely manner).

DNV GL considers the payment milestone and timing requirements of the EPC Agreement to be within industry standard and to provide a reasonable framework for timely completion of the PV systems.

Operations and Maintenance Agreement

For a fee of $23/kW/year (plus escalation), Sunrun (in its contractual role as Operator) will perform maintenance, monitoring, reporting, and administrative functions in support of the commercial operations of the CS V and XV Funds’ portfolio of PV systems. This scope includes major maintenance such as inverter or module replacement. Extraordinary expenses such as system removal, litigation in pursuit of warranty enforcement, and natural disasters and/or regulatory changes, are in addition to the fixed fee.

The terms of the agreements is five years, and are extended in one year increments thereafter as long as a replacement Operator has not been appointed. The OMAs do not stipulate any availability guarantee or performance guarantee; in the absence of a specific performance requirement, it is recommended that the Operator retain an economic interest in the performance of the Funds. In addition to the Ongoing Service Fee, the Operator will be compensated for pursuit of contested warranties, and other items. DNV GL considers the scope and fee arrangements to be well defined for the term of the agreements.

PV System Design and Installation Quality and Portfolio Field Dispatch Statistics

The Sponsor uses third party audits to evaluate ongoing installation quality from its EPC partners. The quantitative inspection scorecard system in use since 2013 has seen steadily improving results, such that more than 70% of all inspected systems in Q2-Q4 2014 meet the Sponsor’s rather rigorous criteria (minimum 85% score and none of 8 priority criteria missed). The CS XV Fund had a 7% inspection rate and a 71% inspection passing rate. DNV GL considers the Sponsor’s inspection scorecard system to be among the best methods in the industry for quantitatively evaluating installation quality, however as evidenced by the checks for the CS XV Fund, the findings which have resulted from these inspections have seen follow through in most but not all cases.

DNV GL has also independently sampled design documentation from 15 PV systems from the Portfolio. The completeness of documentation for these systems’ design and installation varied by contractor and by time of installation, which is consistent with DNV GL’s expectations given that the Sponsor’s latest EPC requirements were not in place for a majority of the sampled systems. Where design or installation issues may impact PV system output (e.g. shading, or poorly sized/connected strings), these examples are included in the production data and so are accounted for in the DNV GL production assessments to the extent they do not worsen over time. The Sponsor has recently made some improvements to its processes. More recent samples of Sunrun projects have been found to include more-thorough documentation, particularly in the form of as built photos. The Sponsor can mitigate this risk via ongoing customer service, maintenance, monitoring and remediation on an as-needed basis. Based on the limited information in this sample set, DNV GL cannot opine on material risk of future structural issues. While omission of this level of review has also been seen elsewhere in the residential solar industry, in order to mitigate risk of future issues DNV GL recommends that the Sponsor implement some process checks in order to ensure that installers are compliant with both code and industry best practices.

The CS V Fund was built prior to implementation of the Sponsor’s current quantitative inspections process. DNV GL has reviewed field dispatch records for the Sunrun fleet, as well as records specific to the CS V and CS XV Funds. Based on the field service history, DNV GL noted that the CS V Fund also had issue frequencies in certain categories (e.g. system failure, system maintenance, and underperformance) slightly above the fleet average in its first year of operation (2012), but equal to or slightly lower than those of the fleet average in 2013-2015. This is seen as a positive indication that the CS V Fund does not have above-typical rates of field service needs, and has achieved a certain degree of operating maturity. The CS XV Fund has had above-typical rates for field service dispatches to date, principally due to problems related to ABB arc fault circuit interrupters.

Financial Model

DNV GL has performed a Monte Carlo simulation of potential performance guarantees for the CS V and XV funds over a 20 year term, using actual system-specific performance history (where available) and/or the distribution of correction factors for each region. The median expected payout was approximately $100,000 per year for CS V and approximately $350,000 per year for CS XV, with such payouts modeled to be generally lower in earlier years and increasing somewhat over time, principally due to DNV GL’s base case assumption of 0.75%/year degradation vs. Sunrun’s guarantee of 0.5%/year output decline.

DNV GL considers the Sponsor’s O&M Agreement fixed fees to be within the range observed in the industry for their scopes of services. The Sponsor has provided a categorized estimate for its 2015 expenses (an annualized $26/kW/year in Q1 declining to $23/kW/year by Q4), as well as well as a pro forma budget estimate of $20.7/kW/year which reduces overhead expenses from the Q4 annualized budget by 20%; the Sponsor has advised that it believes these cost savings would be achievable if it were a servicer which did not engage in origination activities. While DNV GL considers the fixed fee amounts to appear reasonable for such sponsor-provided services and within the range observed in the industry, even after factoring in the projected cost savings there is some risk that the Sponsor’s actual costs may again exceed the fixed fee in the years where 3G network retirements occur or in the event of a significant volume of string inverter replacements in the post-warranty period (years 11+).

DNV GL has also provided stress case guidance with respect to underperformance and O&M costs, and understands that such stress cases have been used by the ratings agencies in their ratings process for the Portfolio.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the reporting entities have duly caused this report to be signed on their behalf by the undersigned hereunto duly authorized.

Sunrun Solar Owner V, LLC (Depositor)

By: Sunrun Inc., its Managing Member

Date: June 19, 2015

| /s/ Mina Kim |

| Mina Kim, General Counsel |

Sunrun Solar Owner XV, LLC (Depositor)

By: Sunrun Solar Owner Holdco XV, LLC, its Managing Member

By: Sunrun Inc., its Managing Member

Date: June 19, 2015

| /s/ Mina Kim |

| Mina Kim, General Counsel |